The revised 2023 budget themed “Building Malaysia Madani” emphasized on ensuring the budget is inclusive and sustainable for economic growth. The budget builds upon three pillars, namely “Inclusive and Sustainable Economic Growth”, “Institutional Reforms and Good Governance to Restore Confidence” and “Social Justice to Bridge Inequality”.

There are a few changes affecting individuals, which are:

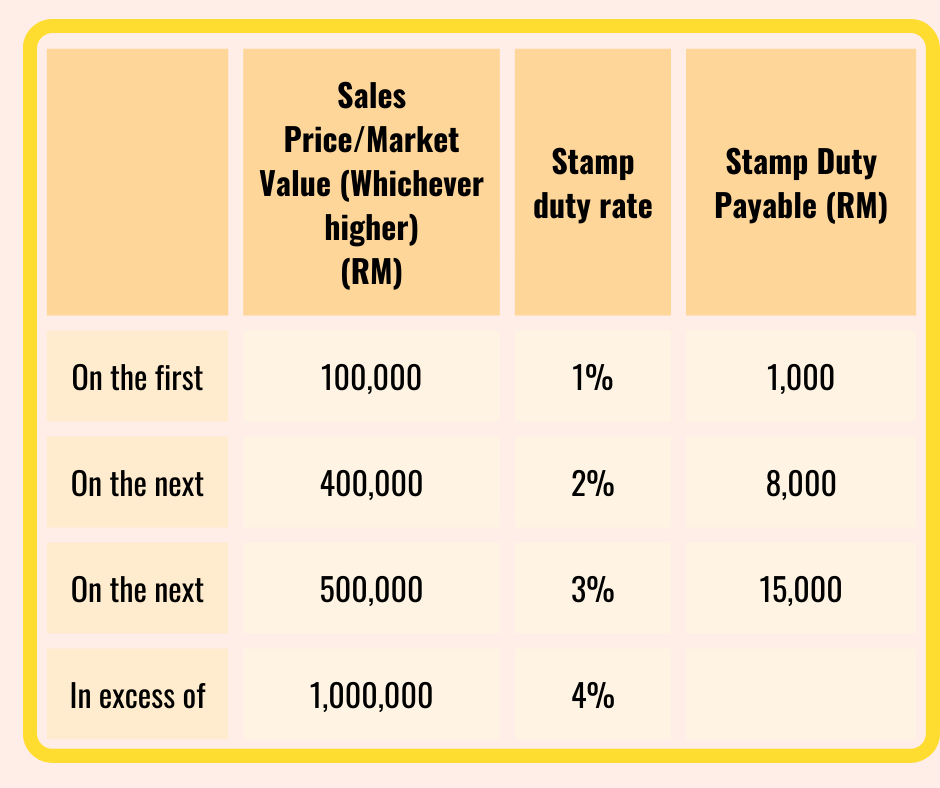

1. Stamp Duty for Transfer of Property by Way of Love and Affection

Existing

Effective 1 January 2019, the stamp duty rates on property transfer are as follows:

A remission of 50% of stamp duty chargeable is given on the instrument of transfer of property executed between parent and child of Malaysian citizenship.

Proposed

1. 100% exemption limited to the first RM1 million of the property’s value

2. The amount in excess of RM1 million in subject to ad valorem duty rate and is given a remission of 50% of the stamp duty chargeable

3. Extended to transfer of property between grandparent and grandchild

This is effective for instrument of transfer of property executed from 1 April 2023 and only applies to a property recipient who is a Malaysia citizen.

2. Tax Relief for Medical Expenses for Self, Spouse and Child

Existing

Tax relief of up to RM8,000 is given to an individual taxpayer for medical expenses with receipts issued by a hospital or a medical practitioner registered with the Malaysian Medical Council (MMC).

The eligible medical expenses include:

1. Treatment of serious diseases (*do refer to IRB website for the list of serious diseases) for self, spouse and child.

2. Fertility treatment for taxpayer and spouse

3. Vaccination for self, spouse and child limited to RM1,000 (* Applicable for certain vaccination)

4. Complete medical examination, mental health examination or consultation and Covid-19 detection text expenses supported with receipts for taxpayer, spouse and child limited to RM1,000

Proposed

1. The tax relief for medical expenses scope be expanded to include early intervention expenditure for Autism, Attention Deficit Hyperactivity Disorder (ADHD), Global Developmental Delay (GDD), Intellectual Disability, Down Syndrome and Specific Learning Disabilities limited to RM4,000 for:

>> Diagnostic assessment certified by a medical practitioner registered with the MMC

>> Early intervention and rehabilitation programmes conducted by health profession practitioners registered under the Allied Health Profession Act 2016

It is aimed to ease the financial commitment on early intervention for children with learning disabilities.

2. The amount of tax relief for medical expenses be increased from RM8,000 to RM10,000.

This is effective from year of assessment 2023.

3. Extension of Tax Relief for Child Care Centre

Existing

Tax relief of RM3,000 is given to taxpayer (either parent of the children) who enroll their children aged 6 years and below in Child Care Centres (TASKA or TADIKA) registered with the Social Welfare Department or Ministry of Education Malaysia from year of assessment 2020 to 2023.

Proposed

The tax relief for child care centre will be extended up to year of assessment 2024.

4. Restructuring of Tax Relief for Life Insurance Premium or Takaful Contribution

Existing

Proposed

5. Stamp Duty Exemption for the Purchase of First Residential Property

Existing

A full (100%) stamp duty exemption is given on instrument of transfer and loan agreement executed from 1 January 2021 to 31 December 2025 for the purchase of first residential property valued to up RM500,000 by a Malaysian citizen.

50% stamp duty exemption is given for property valued between RM500,001 to RM1,000,000 executed from 1 June 2022 to 31 December 2023 under the Keluarga Malaysia Home Ownership Initiative (i-MILIKI).

Proposed

The stamp duty exemption for property valued between RM500,001 to RM1,000,000 is revised from 50% to 75% subject to the following conditions:

(a) The residential property is purchased through the Malaysian Home Ownership Initiative (i-Miliki) under the Home Ownership Programme 2022/2023

(b) The sale and purchase agreement (SPA) is between an individual and a property developer

(c) The purchase price in the SPA is the price after a discount of at least 10% from the original price offered by the property developer, except where the residential property is subject to controlled pricing

(d) The SPA is executed between 1 June 2022 and 31 December 2023, and is duly stamped no later than 31 January 2024

(e) The individual has never owned any residential property, including a residential property obtained by way of inheritance or gift, which is held either individually or jointly.

All information, materials, content and/or advice in this article is for informational purposes only and is not intended to replace or substitute for any professional advice.