The revised 2023 budget themed “Building Malaysia Madani” emphasized on ensuring the budget is inclusive and sustainable for economic growth. The budget builds upon three pillars, namely “Inclusive and Sustainable Economic Growth”, “Institutional Reforms and Good Governance to Restore Confidence” and “Social Justice to Bridge Inequality”.

There are a few changes affecting SMEs, which are:

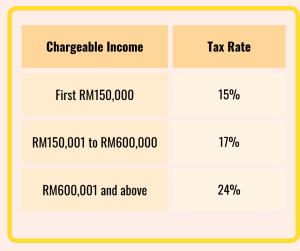

1. Income Tax Rate for Micro, Small and Medium Enterprises (MSME) which are Companies

A company is a MSME if it is:

a) a resident company incorporated in Malaysia with a paid-up capital in ordinary shares of up to RM2.5 million at the beginning of the year of assessment;

b) Annual gross income not exceeding RM50 million; and

c) Not more than 50% of paid-up capital in respect of ordinary shares are owned directly or indirectly by a related company which has a paid-up capital in respect of ordinary shares of more than RM2.5 million at the beginning of the year of assessment.

Effective from year of assessment 2023, the income tax rate are:

However, effective from year of assessment 2024, if a Company with 20% of its paid-up capital in respect of ordinary shares at the beginning of a year of assessment is directly or indirectly owned by one or more companies outside Malaysia or individuals who are non-Malaysian citizens will not enjoy the tax rate of MSME above.

2. Tax Deduction to Hoteliers for Expenditure Incurred on Malaysian-Made Handicraft

Existing

A company who incurs qualifying capital expenditure is allowed to claim capital allowance under Schedule 3 of the Income Tax Act 1967.

Subsequent purchase for replacement of an asset valued at less than RM2,000 is given tax deduction under Section 33 of the Income Tax Act 1967.

However, there is no clear guidance as to whether the expenditure incurred by hotelier on purchasing Malaysian-made handicraft products as display items at the hotel premises qualifies as “plant” for capital allowance claiming purpose.

There is also no special tax deduction in purchasing Malaysian-made handicraft as such expenditure is not revenue expenditure.

Proposed

A special tax deduction of up to RM150,000 is given to hoteliers in respect of expenditure incurred on

i) Malaysian-made handicraft

ii) Purchased from local handicraft entrepreneurs registered with the Malaysian Handicraft Development Corporation (Perbadanan Kemajuan Kraftangan Malaysia)

iii) For display at hotel premises

This special deduction is not applicable if the hotelier has claimed for tax deduction under Section 33 of the ITA 1967 or claimed capital allowance under Schedule 3 of the ITA 1967.

This is effective for eligible expenditure on handicraft products incurred from 1 January 2023 to 31 December 2025.

3. Tax Deduction for Rental of Non-Commercial Electric Vehicle (EV)

Existing

Rental of non-commercial motor vehicles are restricted to the amount of tax deduction under Section 39(1)(k). Depending on the cost of the vehicle when new, the maximum amount deductible are:

Proposed

For non-commercial EV, the maximum rental amount allowable for tax deduction is restricted at RM300,000.

This is effective for year of assessment 2023 to 2025.

4. Tax Deduction of Employment of Senior Citizen (60 years and above), Ex-convict, Parolee, Supervised Person and Ex-Drug Dependant

Existing

A further tax deduction is given to employers who employ senior citizens, ex-convicts, ex-drug dependants and convicts who are categorised as parolees and supervised persons, subject to the following conditions:

(a)The employee is employed on a full-time basis;

(b)The monthly remuneration does not exceed RM4,000;

(c)The employer and employee are not the same person; and

(d)The employer is not a relative of the employee

This tax incentive is given until year of assessment 2025

Proposed

The above further deduction be expanded to include remuneration paid to inmates and ex-inmates of:

(i)Henry Gurney School under Malaysian Prison Department

(ii)Protection and rehabilitation institutions and non-government care centres registered with the Department of Social Welfare

This is effective for year of assessment 2023 to 2025.

5. Implementation of Electronic Invoicing System (E-Invoicing)

The Government plans to make e-invoicing a mandatory requirement in the following phases:

Year 2023 – Development of infrastructure and pilot projects with selected companies

June 2024 – Mandatory for businesses achieving sale threshold of RM100 million a year

January 2025 – Mandatory for businesses achieving sale threshold of RM50 million a year

January 2026 – Mandatory for businesses achieving sale threshold of RM25 million a year

January 2027 – Mandatory for all businesses

Voluntary implementation of e-invoicing is allowed with effect from 1 January 2024.

6. Review of Tax Incentive on Automation Equipment

Existing

Qualifying capital expenditure on automation equipment incurred by manufacturing and services companies may be eligible for:

(a)Accelerated capital allowance (ACA) of 100%

(b)Income tax exemption of up to 70% of statutory income derived from the qualifying project at 100% of the ACA

Conditions:

(a) The automation equipment is required to be certified by the Standards and Industrial Research Institute of Malaysia (SIRIM)

(b) Available from year of assessment 2015 until year of assessment 2023 for applications received by Malaysian Investment Development Authority (MIDA)

Proposed

The tax incentive be enhanced as follows:

1. Scope of automation to include adaption of Industry 4.0 elements

2. Scope of qualifying project be expanded to include agriculture sector

3. Maximum qualifying capital expenditure for all qualifying projects be increased to RM10,000,000

This is effective for applications received by MIDA and Ministry of Agriculture and Food Security (MAFS) from 1 January 2023 until 31 December 2027.

All information, materials, content and/or advice in this article is for informational purposes only and is not intended to replace or substitute for any professional advice.