Malaysia is one of the latest country to introduce e-invoice which is a digital representation of a transaction between a supplier and a buyer and replaces paper or electronic documents such as invoices, credit notes, and debit notes to support the growth of digital economy.

So, what is e-Invoice and how does it impact you as a taxpayer?

We will briefly discuss e-invoicing based on the E-Invoice Guideline (Version 1.0) issued by Inland Revenue Board of Malaysia (IRB) on 21 July 2023. (Updated Version 2.2 published on 9 February 2024)

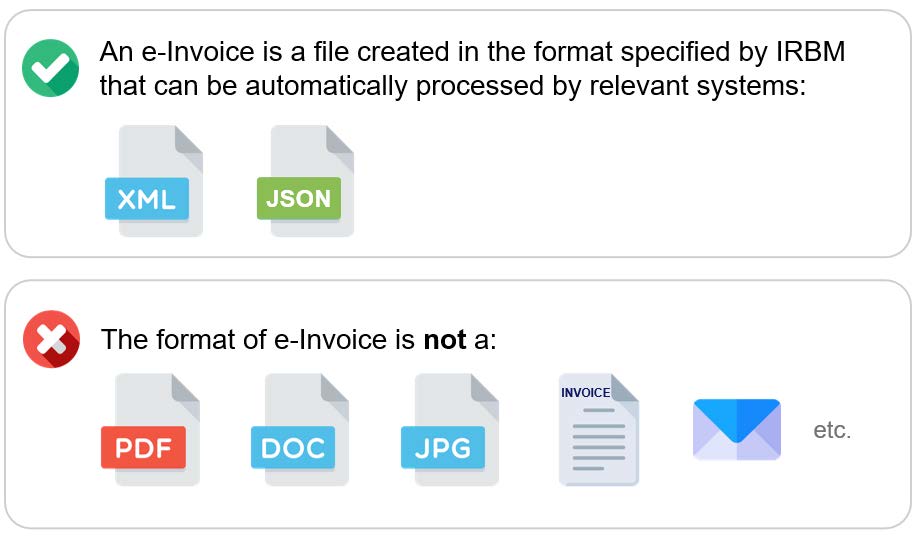

An e-Invoice contains the same essential information as traditional document, for example, supplier’s and buyer’s details, item description, quantity, price excluding tax, tax, and total amount, which records transaction data for daily business operations.

An e-Invoice contains the same essential information as traditional document, for example, supplier’s and buyer’s details, item description, quantity, price excluding tax, tax, and total amount, which records transaction data for daily business operations.

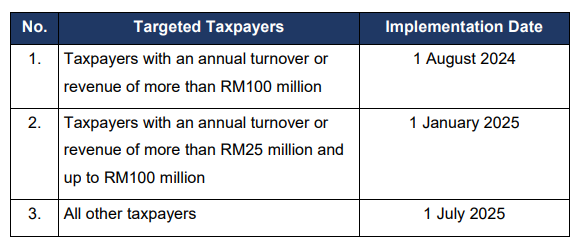

Timeline

E-invoice will be made mandatory for all taxpayers on 1 July 2025 and businesses will need to have their information technology and system to be ready before that date.

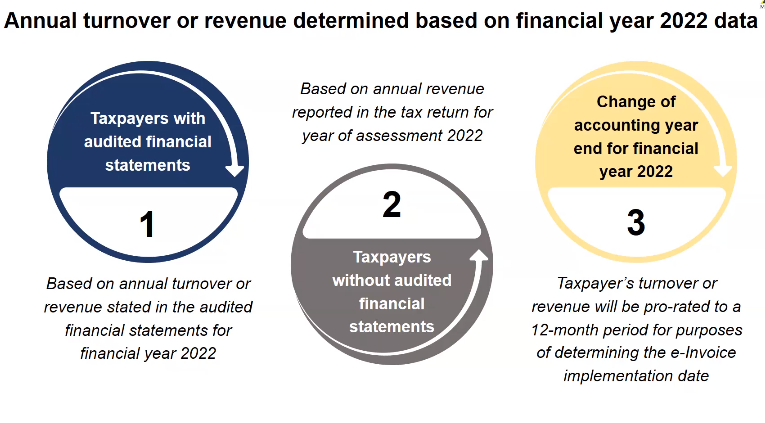

However, the mandatory implementation date will be earlier if you business falls under the following targeted category based on annual turnover or revenue which is determined based on 2022’s audited financial statements and tax returns.

The implementation timeline will not be changed in subsequent years even if there is any changes to the taxpayer’s annual turnover or revenue.

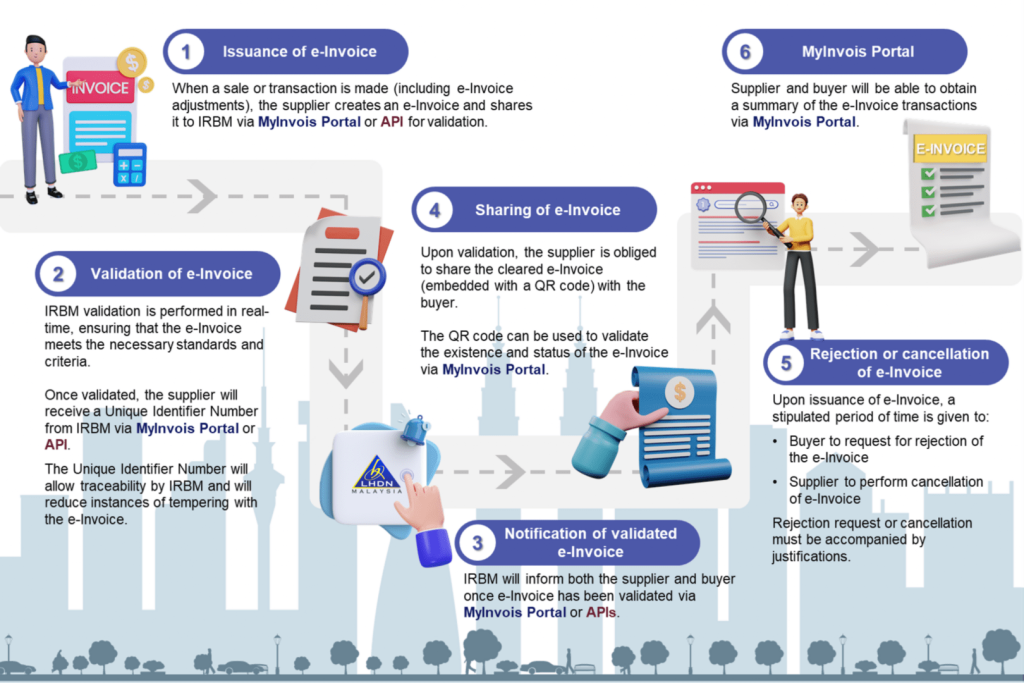

Overview of E-Invoice workflow

E-Invoice Model

Taxpayer can select either the following 2 mechanisms to transmit e-Invoice to IRBM depending on the suitability.

a. A portal (MyInvois Portal) hosted by IRBM

b. Application Programming Interface (API)

![]()

Compliance

E-Invoice applies to all taxpayers undertaking commercial activities in Malaysia including certain non-business transactions between individuals and international transactions. Guidance on e-Invoice requirements for certain non-business transactions between individual taxpayers will be provided in due course.

All individuals and legal entities are required to comply with e-Invoice requirement, including:

1. Association;

2. Body of persons;

3. Branch;

4. Business trust;

5. Co-operative societies;

6. Corporations;

7. Limited liability partnership;

8. Partnership;

9. Property trust fund;

10. Property trust;

11. Real estate investment trust;

12. Representative office and regional office;

13. Trust body; and

14. Unit trust.

Business to Consumer (B2C)

IRB has mentioned in the guide in which certain B2C transactions where e-Invoices are not required by the end consumers to support the said transactions for tax purposes, suppliers will be allowed to issue a normal receipt or invoice in accordance with the current practices adopted by suppliers.

After a certain period or time frame, suppliers would be required to aggregate the normal receipts or invoices issued to end

consumers and issue a consolidated e-Invoice to support the transactions made with end consumers. Further guidance on this will be provided in due course by IRB.

![]()

What can you do now?

As suggested by IRB, here are a few key steps that can be carried out to assess readiness and standardisation:

1. Allocate and equip personnel with the necessary capabilities to adopt and oversee the implementation of e-Invoice;

2. Determine availability of data sources and structure, current IT capabilities to support system readiness and processes to comply to e-Invoice requirements and obligations; and

3. Review current processes in issuing transaction documents (i.e., invoice, debit note, credit note, refund).

Question regarding E-invoice?

You can always reach out to IRB via myinvois@hasil.gov.my or refer to the full version of the guideline here.

All information, materials, content and/or advice in this article is for informational purposes only and is not intended to replace or substitute for any professional advice.